We previously talked about the formula for valuation and the importance of growth in these formulas:

Valuation = EBITDA x EBITDA multiple (low growth rate company)

Or

Valuation = Last 12 month revenue x Revenue multiple (high growth rate company)

Growth rate is arguably the most important factor in the multiplier but the multiplicand in a high growth company is the revenue. Growth rate is growth in revenue but growth rate indicates future potential, which leads to a high multiple. Revenue is a metric of where the company is today and impacts both the multiplier and multiplicand. This post covers why revenue is such an important driver of value.

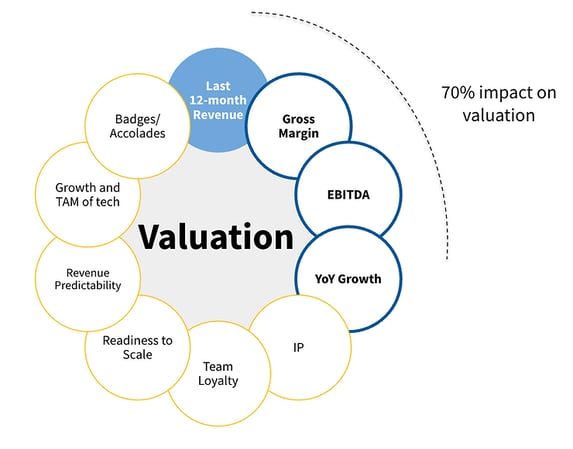

Valuation Drivers

Valuation Drivers

1. Revenue determines the base multiplier

Fundamentally, higher revenue means lower risk for an acquirer. While it is not a universal truth, larger companies are more robust and revenue is one of the strongest indicators of size – thus robustness. Larger companies have structures and capabilities built in to ensure continued value for the acquirer. Thus, companies are often T-shirt sized based on their revenue. Small ETS companies with under $1mm in revenue get lower base multipliers (0.5x-1x) and larger ETS companies with $10mm+ in revenue get bigger base multipliers (5-6x). The base multiplier is then adjusted based on other factors and drivers. But, all in all ,revenue and growth are typically the starting point of any valuation discussion. We will write a more detailed blog post in the coming months to explain typical T shirt sizes and revenue multiplies that we have seen.

2. It is used to compute your Opportunity Cost

When considering any option there is always the option to not do anything. In the same way when you are looking to get acquired, your company is first and foremost compared against the opportunity cost of it you decided to just run the business. The four major drivers of valuation (revenue, gross margin, EBITDA, and growth rate) cumulatively represent the opportunity cost of running the business. And this opportunity cost is captured in the company valuation formulas. The most important, hardest to manipulate number is revenue. EBITDA does not work for high growth companies because of the cost of growth. Growth itself is a prediction and can come crashing down because of the chasms. The gross margins are useful in determining the quality of the revenue but can be manipulated. The revenue, however, is king.

A strategic buyer may value many things in a potential acquisition. Adding in new accreditations, expertise, customer offerings, customers to cross-sell to. But they will bid based on your opportunity cost as represented by the formula. You can get some credit from other features and start a bidding war but your revenue represents the starting point of the bidding war. Even if a business unit recognizes the value, having a large M&A deal requires getting approval from the finance department which will again evaluate the business being purchased as a business rather than the value potential. Taking us back to the revenue formula.

3. It is a proxy for Head Count and quality of talent

One of the major things a buyer is looking for in buying an ETS is the head count of delivery engineers. A buyer usually has their own operations like HR, accounting and other functions. But the revenue generating staff represent the strategic expertise they are trying to acquire. Acquiring this expertise in-house is the main reason a strategic acquirer is looking to purchase an ETS firm. So your revenue is a simple proxy for how far along your company will take them to building the practice. Your revenue represents that you have people and they are good enough that customers are paying for their skills.

4. It shows your market share

One reason the revenue is very valuable to an acquirer is because ETS startups are in a land grab phase. The conventions for the technology are in the process of being defined. The early winners will forever be the first which is the best time to win deals rather than in trying to displace incumbents. So ETS are in a land grab phase. Trying to become the definitive partner for customers. Your revenue represents how successful you have been at your land grab and represents the stronghold of future customer revenue they are buying.

Side note: Not all revenue is created equal. There is a concept of revenue quality which has an impact on the multiplier as well and not all revenue is treated the same when it comes to valuations. Factors that influence revenue quality include concentration (revenue from many customers is better than just one), stickiness (revenue that is promised versus revenue that has to be earned regularly), and gross margin (revenue that produces higher gross margins is more valuable). We will cover this topic in detail when we write about the value driver we call Revenue Quality.

At Vixul, we believe Revenue and Growth rate are the strongest indicators of an ETS’ success. The Vixul Maturity Framework has a deep focus on helping our startups increase both. Learn more about Vixul and our mission at vixul.com.

The other articles in our "Demystifying ETS Valuations" series are:

-

Demystifying ETS Valuations Part 4: EBITDA and the rule of 40

-

Demystifying ETS Valuations Part 5: Intelectual Property

-

Demystifying ETS Valuations Part 6: Addressable Market

-

Demystifying ETS Valuations Part 7: Revenue Predictability

-

Demystifying ETS Valuations Part 8: Team Loyalty

-

Demystifying ETS Valuations Part 9: Badges And Accolades

-

Demystifying ETS Valuations Part 10a: Readiness To Scale

-

Demystifying ETS Valuations Part 10a: Readiness To Scale